In my previous post, I shared about achieving Full Retirement Sum (FRS) in CPF Special Account (SA) as early as possible to take advantage of the compounding effect.

The next question you may ask is how?

Looking back, I deployed a combination of strategies to meet the goal. Honestly, I was surprised that I have topped up >$30K cash into my SA (over 7 years), a considerable sum to put aside till 55.

For anyone embarking on this journey, it certainly looks daunting. Having experienced similar doubts like many others before me, I would like to share my personal experiences and much needed convictions that helped me achieved my goal.

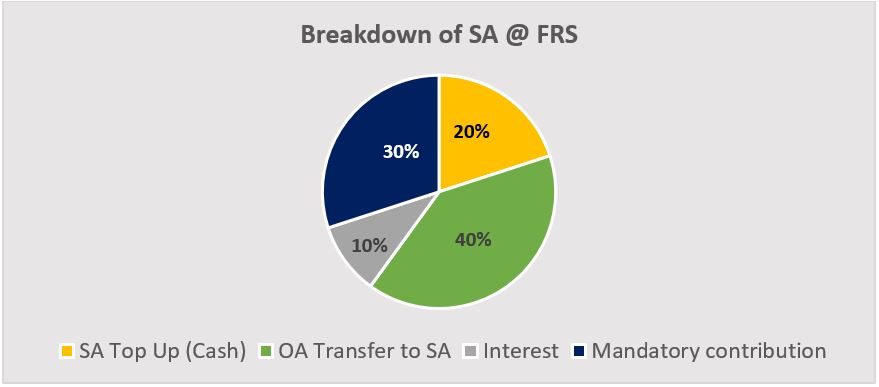

Snapshot of CPF Special Account

Let’s dive right in and analyse the breakdown of my SA account when I achieved FRS ($181K). Less than half of FRS was from mandatory salary contribution and interest. The remaining FRS was accumulated through active transfers via cash top-ups to SA (20%) and OA transfers (40%). This did not happen overnight but in tranches and with careful planning – it took me 7 years to achieve this since my first cash top-up.

How it all started…

I did not conceive the idea of achieving FRS in SA right from the start. It was over a period of time that my conviction grew and gave me the confidence to achieve this goal.

Additional 1% CPF interest for first $60K

My original intent to top up my SA was to take advantage of the additional 1% CPF interest for first $60K in OA and SA (capped at max $20K in OA). At a point in time, my OA exceeded the $20K limit but SA was way below $40K. Hence, to take full advantage of the additional interest in SA, I started making cash top-ups to SA for a few years. Furthermore, it also helped that I could get income tax reliefs, an additional incentive, for CPF top-ups.

Glimmer of Hope: CPF Millionaire

After hitting 40K in SA which ‘maxed’ out the additional interest, I needed more conviction to keep going. It got me really excited when I chanced upon the possibility of achieving $1M in CPF through forums, blogs and the 1M65 movement by Mr Loo Cheng Chuan. CPF seemed to be a more realistic tool (than striking lottery) towards achieving $1M.

Inspired, I performed some calculations and realised it was indeed mathematically possible. It was quite an eye-opener and motivated me towards achieving FRS as soon as possible. From my simulations, it was evident that monthly mandatory salary contributions would not suffice.

Even though making cash top-ups to SA helps, there was still much room to grow to achieve a moving FRS target (FRS has been increasing at ~3% for the past few years). I needed to couple this with another strategy to bridge the gap.

Biting the bullet

Another strategy to meet FRS in a shorter period of time is to transfer from OA to SA.

It was around the time when my flat was ready and I knew that my OA will be wiped out to pay for it (note: flat buyers can now keep $20K in OA). After much procrastination till a few days before key collection, I decided to bite the bullet and transferred a 5-figure sum from my OA to SA. This was the tipping point that significantly boosted my SA.

Obviously, it was not an easy decision even with the extensive research and preparation done. The doubts about having the funds locked up and uncertainties of future policies constantly challenged my conviction. In fact, those uncertainties are still valid today because nobody can predict what will happen. However, as with many things in life, do weigh risk and reward to make judgement accordingly.

Turbo-charge

After making the ‘big’ decisions, the following years of account management have been as planned . Each year, I do cash top-ups and transfer any excess balances from my OA and I find myself logging into CPF more often to watch the funds grow. After doing my sums further, I also started paying my mortgage with cash and transferred the balance from OA to SA each month till it meets FRS.

In Summary

Achieving FRS in SA requires discipline, conviction and commitment. It is one of my major milestones towards financial freedom. I see it as my safety net for retirement because even if I stop working now, the yearly interest from SA should be sufficient to meet or exceed the annual increase in FRS. This means that I have secured a reasonable monthly pay-out from CPFLife when I turn 65 (equivalent to $1,390 – $1,490/month based on 2020 estimates).

Please take note that I am sharing my personal experience and strategies and this is not an advice for you to follow as everyone has different background/experiences/circumstances. The key is to find your conviction, plan and take action early to maximize the compounding effect.

To share the tool I used to strategize my deployment of funds with Singaporeans exploring similar possibilities for themselves, I have developed a CPF calculator which could come in handy. If you like to project and simulate your CPF balances, click here to get the free CPF Calculator. I would encourage you to do the same due diligence too to get the conviction required.

The journey of a thousand miles begins with one step – Lao Tzu