We have often heard about the term Retirement Planning but what does it really means? There are many ways to plan for retirement but let me share my thoughts around this topic pertaining to CPF.

What does a CPF Retirement Plan entails?

- I have a plan of when (at what age) I can have the option to retire

- I have the financial means to sustain my lifestyle when I choose to stop working

I am able to have more clarity to the above 2 questions after I ‘maxed out’ prevailing CPF Special Account’s (SA) Full Retirement Sum (FRS) and Medisave Account’s (MA) Basic Healthcare Sum (BHS) as early as possible.

By optimizing SA and MA accounts as early as possible, I can allow both accounts to compound at 4% annually (prevailing interest rates).

At age 55, after the Retirement Account (RA) has been set up, the remaining amount in my SA and OA can be withdrawn at any time. I can choose to leave them in their respective accounts to earn 2.5% (OA) and 4% (SA) interest annually which I can start to draw down should I wish to semi-retire.

At age 65, my passive income would be supplemented by monthly CPF Life payouts and the option of full retirement is highly probable. CPF should not be my only retirement asset eventually but it will be the first asset to focus on to leverage the power of compounding given that its more stable vs other assets.

Leverage Compounding

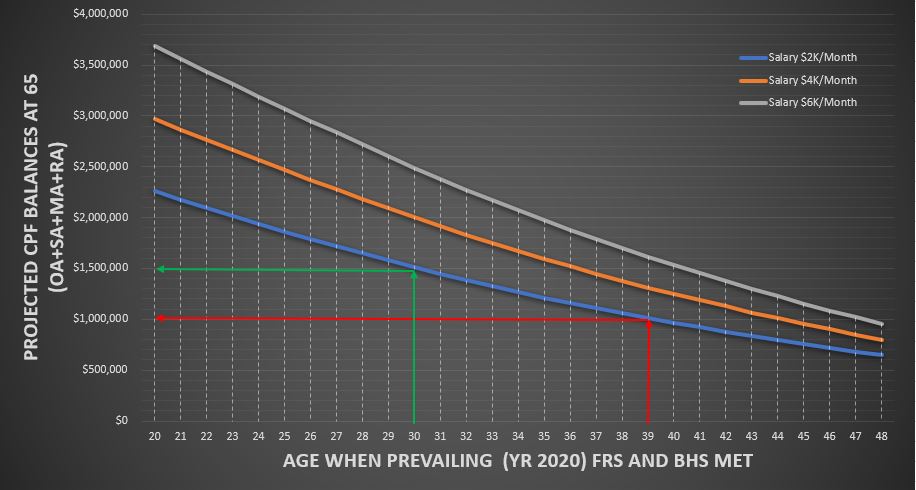

To illustrate the compounding effect of ‘maxing’ out the accounts as early as possible, refer to below chart on the projected CPF balances at 65 against respective Age whereby prevailing SA’s FRS ($181K) and MA’s BHS ($60K) has been reached.

From the chart, it is clear that the earlier (to the left of the chart) we achieve FRS and BHS respectively, the higher our projected total balances in CPF will be and hence a better chance of retirement.

For example:

With monthly salary of $2K/month and achieving FRS & BHS at age 39, total balances at 65 will be ~$1M. However, if FRS & BHS are achieved at age 30, total balances at 65 will be 50% more at ~$1.5M. Note the following assumptions used in the projections: $0 in OA at the start of projection, salary is constant and no salary bonus.

Key Points:

- Start planning for retirement early (not in our 50s or 60s, it is too late!)

- Actively plan for retirement by topping up cash to SA and transferring from OA to SA to ‘max’ out the accounts to prevailing FRS and BHS.

- After achieving FRS and BHS, as long as I continue working and CPF policies do not change drastically, the power of compounding will work its magic. (Tip: if you have achieve FRS ($181K) and BHS ($60K), their total interest at 4% is at least $9.6K every year!)

- Compounding only works if given enough time. While we are slogging hard it work, don’t let time slip by. Let time work for us by compounding early!

- Having a retirement plan doesn’t mean I will stop working but it is the freedom to stop working when I want to, without having to worry about the regular income stream.

Check out the free CPF Calculator to start planning 🙂

Thanks for reading.